You are here

Back to topFDK China Market Update — Week 13

March 31, 2026

This newsletter is published on behalf of Fruit Data Kings, a Berlin-based company specializing in pricing data and associated analytical tools for the fresh produce industry. For more information, visit the Fruit Data Kings website.

Apples (⇩)

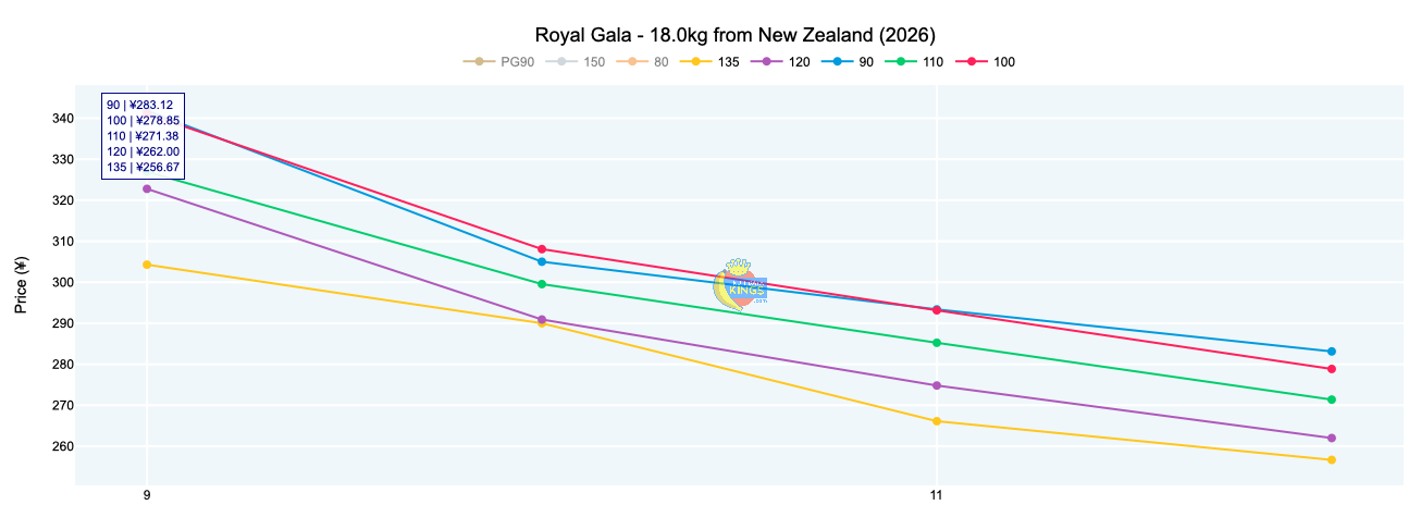

New Zealand continues to account for the vast majority of apple openings in southern China, with Royal Gala the leading variety at over half of recorded activity. Pricing has been on a steady decline over the past month, easing from an average value of ¥330 four weeks ago to ¥269 this week (18 kg, various sizes). At this value, we are slightly below the 2024 level but firmer than the same week of 2025. Initial arrivals of other South African goods have been received, while the vast selection of varieties out of New Zealand are gradually making their way into the market. Full details can be viewed online.

Avocados (⇧)

Imported avocado pricing lifted slightly this week, with Peruvian goods rising by ¥5 to ¥10 compared with week 12. Presently, Peruvian Hass avocados are mostly moving in the region of ¥115–130 (4 kg, various sizes) with an average value of ¥122 (4 kg). At the retail level across notable retailers, we record an average price of ¥64 per kilogram, which is visibly lower than the same week of 2025.

Blueberries (⇩)

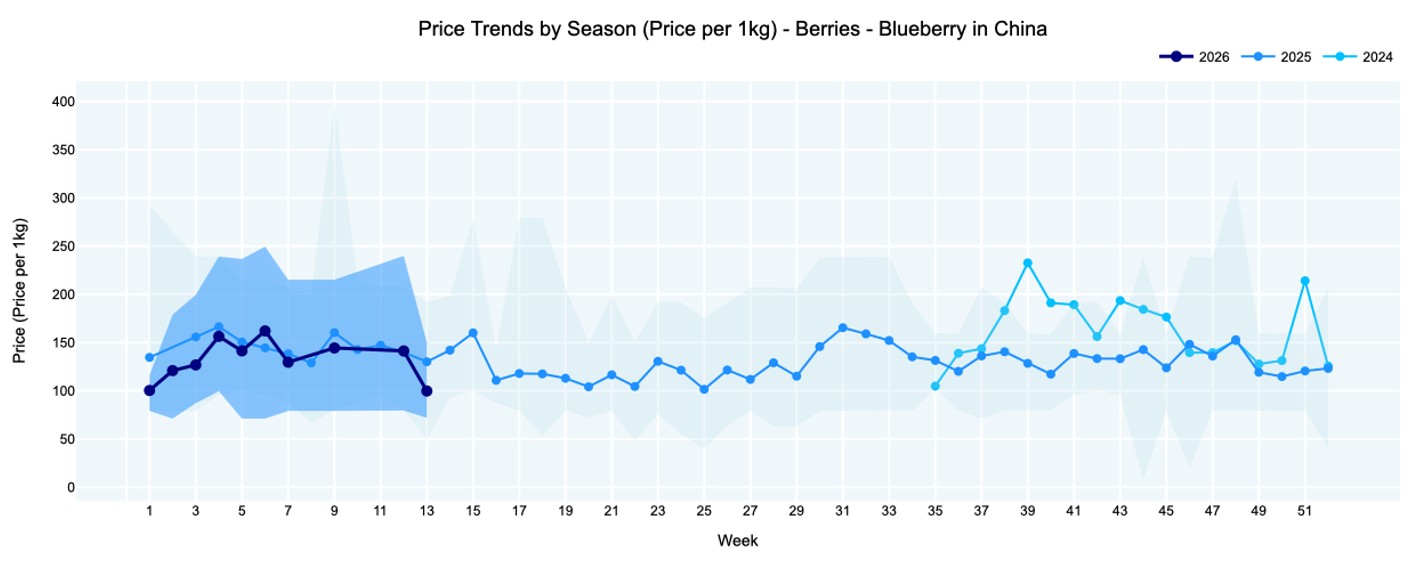

Domestic supply remains vibrant with Yunnan, Guangdong and Sichuan blueberries all available. Blueberry pricing declined this week, with Yunnan L11 trading between ¥60 and ¥90 (1.5 kg, 15/18+ mm) and L25 between ¥60 and ¥95 (1.5 kg, 15/18+ mm). Supply from Sichuan was priced at a visible premium compared with Yunnan. Retailer pricing was sitting at an average of ¥12.50 (125 g). Further details are available online.

Grapes (⇨)

Crimson, Sweet Globe, Autumn Crisp and Sable are all rather dominant varieties over the past three weeks. Australian Crimson remained rather steady in price this week, averaging at ¥267 (9.5 kg), which is about 15% above the same week of both 2024 and 2025. Chilean Sable traded at ¥149 (8.2 kg, various sizes), broadly in line with 2025 but well below 2024. Chilean Red Globe improved in price to average at ¥223 (8.2 kg), about 19% above last year. Full market details covering Peruvian, South African and other varieties are available to members.

Nectarines (⇩)

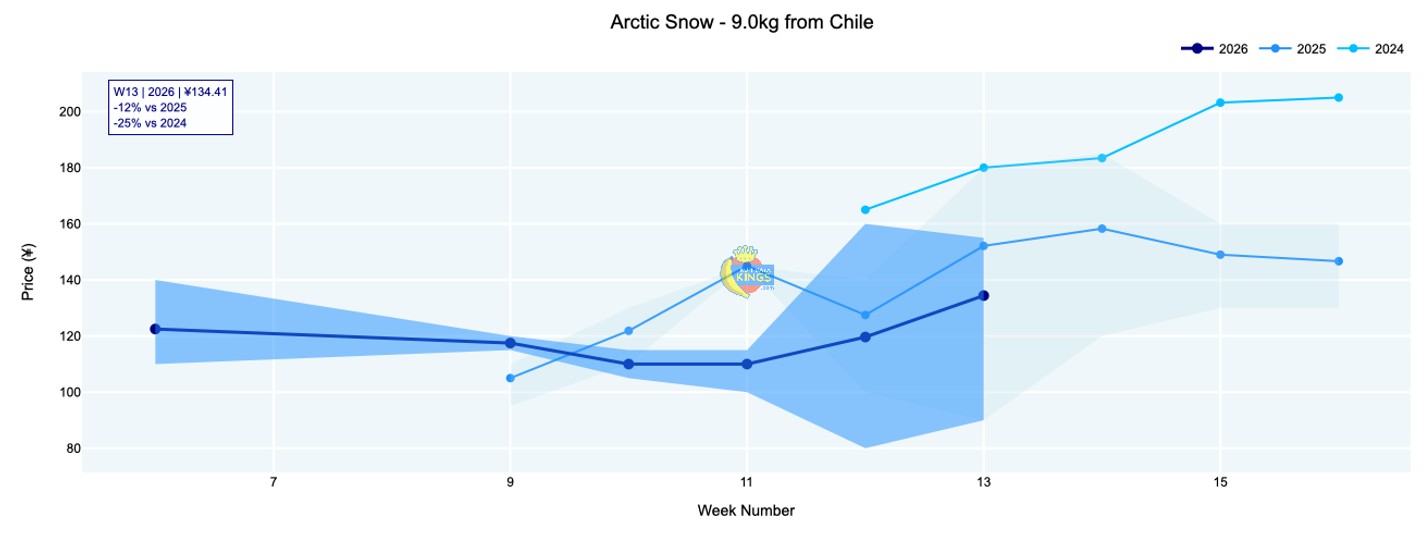

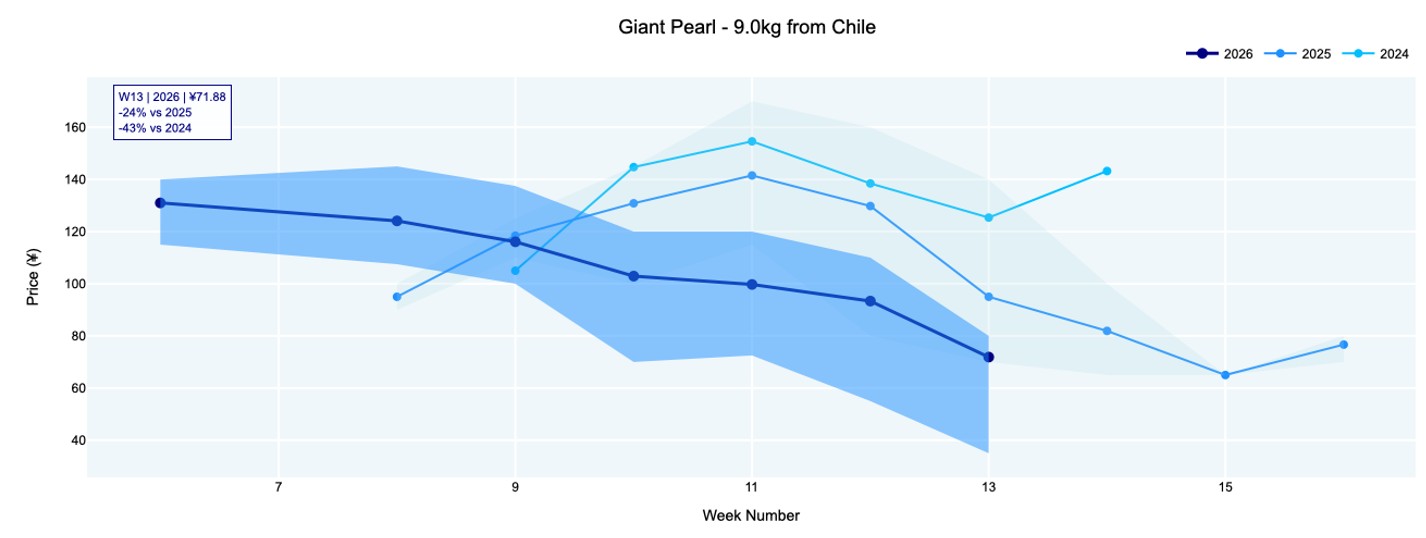

Chilean Sweet Giant held at ¥94 (9 kg, various sizes), about 10% below last year, while Arctic Snow firmed to ¥134 (9 kg, various sizes) after gaining ¥18 compared with last week. Giant Pearl slipped to ¥72 (9 kg), about 24% below 2025 levels. Full year-on-year charts, as well as price by size charts of various varieties, are available online.

Oranges (⇩)

The import market for oranges pulled downward during the week for Spanish, U.S. and Egyptian goods. Currently, Egyptian Valencia oranges are priced approximately 15% lower than last season and 25% lower than 2024. One needs to keep in mind that the higher values of 2024 were tied to Red Sea closures, which carried forward into 2025. Full details are available to members.

Plums (⇩)

Over the past three weeks, sugar plums have continued to dominate the market, followed by Pink Delight and Sweet Mary. Sugar plum pricing stands at around ¥140–150 (9 kg), about 23% below the same week of 2025 but a few percent above 2024. For full specifics, as well as retail pricing, visit us online.

Quick links:

Image: Pexels

Regions:

-

June 29, 2026

-

June 28, 2026

-

June 24, 2026

-

June 22, 2026

-

June 21, 2026

-

June 01, 2026

-

June 08, 2026

-

June 09, 2026

-

June 12, 2026

-

June 01, 2026

Upcoming Events

Produce Marketplace

- ElGhaoutiCrops · Morocco

- Elangeni Food Group · South Africa

- Universal Capital Gr · Ecuador

- wesdTwEobtyBcUzust · HSiKyixhQs

- Hainan ITG Logistics · A26,Haikou

- Joshua Lim · Malaysia

Add new comment